Last week we published the article Turkey - A Study In Keynesianism in which we highlighted the Turkish economy as an example of Keynesianism and the consequences it brings. Today we are going to contrast that study with its opposite, a study of an example of Free Markets… And herein lays the problem. There are no free markets. As such we need to pick a country, any country, which is as close as possible to them. Granted. The comparison won't be pure nor pristine but it will at least allow us to get closer to a living, breathing free-ish market economy and its benefits. For that, we are going to re-calculate all the same economic variables we performed with Turkey and thus contrast the differences. To task.

Last week we published the article Turkey - A Study In Keynesianism in which we highlighted the Turkish economy as an example of Keynesianism and the consequences it brings. Today we are going to contrast that study with its opposite, a study of an example of Free Markets… And herein lays the problem. There are no free markets. As such we need to pick a country, any country, which is as close as possible to them. Granted. The comparison won't be pure nor pristine but it will at least allow us to get closer to a living, breathing free-ish market economy and its benefits. For that, we are going to re-calculate all the same economic variables we performed with Turkey and thus contrast the differences. To task.

THE USUAL AND NOT-SO-USUAL STUFF

To begin with, we don't have the usual political bitching and moaning every time the Singapore Dollar (the SGD) suffers a hiccup. This is so because as we will see, the SGD goes through normal fluctuations which are, for the most part, allowed to be. In this sense this mirrors (more or less) what would happen in free markets because in such markets there would be no Central Banks and real money would fluctuate just a little without much consequence.

THE FUZZ

What the fuzz is all about is how free markets lack the conundrum that Keynesianism and its modern version -Monetarism- are all about (see for example The Impossible Trinity - Or Why Mainstream Economics Sucks and Fake Money For A Fake Economy and Real Money For A Real Economy for a technical explanation). In a nutshell and because the SGD (a fiat currency) is allowed to oscillate, it is not only possible to have the following three properties simultaneously but it actually happens in real life:

- Stable Exchange Rates

- Free Capital Flow

- Independent Monetary Policy

With a twist… Singapore allows for a great deal of flotation and so the Exchange Rates remain more-or-less Stable and because of this there is a fair amount of Free Capital Flow and as the Monetary Policy is minimalistic it can therefore be Independent as it interferes very little with free markets.

THE SHORT TERM

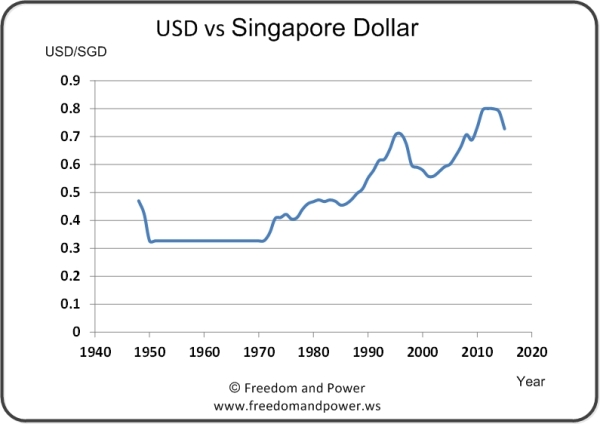

The chart below represents the reason why there are no tantrums coming from politicians in Singapore. As you can see the SGD is fairly stable over time and this creates stable economic conditions which foster stable and easy economic calculations for imports as well as exports… which is to say local manufacturing and local prices. Basically, the economy is stable and resilient even when the world is falling off a cliff as it happened in 2008. And the chart below so indicates.

THE NOT SO SHORT TERM

This holds more-or-less true even if we examine the same chart further back in time (up to 1970!) where we can see no massive short-term variations.

Before 1970 the Singaporean government behaved just like any other government with constant Central Bank interventions which in this case meant pegging the value of the SGD to the GBP and USD (thus the flat line between 1950 and 1970). This had the catastrophic effect of bringing all kinds of economic problems to Singapore. Between 1970 and 1980 however, the Singaporean government progressively adopted the current policy (and things began to change for the better) which is unusual among "developed" nations… to say the least.

Basically, the Singaporean Central Bank does not use any of the "normal" monetarist tools (i.e. interest rate manipulation) but it intervenes in the FOREX market directly to keep the SGD within a band with respect to a basket of other currencies. The main purpose of this intervention is not to prevent the variation of the value of the SGD but simply to smooth the fluctuations. This has the effect of creating a fairly stable SGD valuation over longer periods of time… which is what happens in free markets where the amount of real money remains more-or-less constant over time.

As a consequence of this, Singapore has floating and unregulated interest rates. These rates are determined by the market based on the USD rates (i.e. the Fed in USA) and economic expectations in Singapore and in the world. This is what happens (more-or-less) in free markets where the interest rates are determined purely by the markets based on economic calculations of future economic activity.

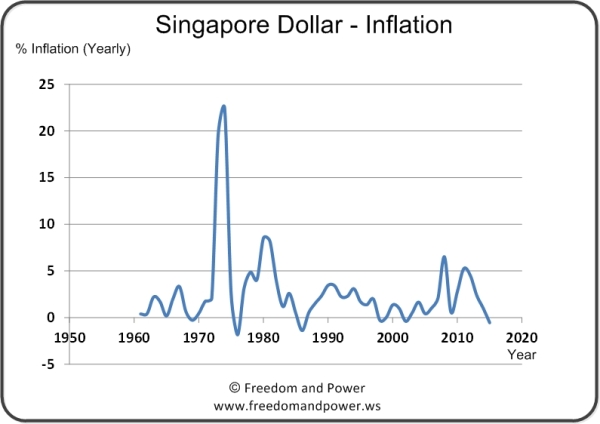

The net effect of these policies is that, in general terms, inflation is kept low and stable:

AND THE ECONOMY IS OK

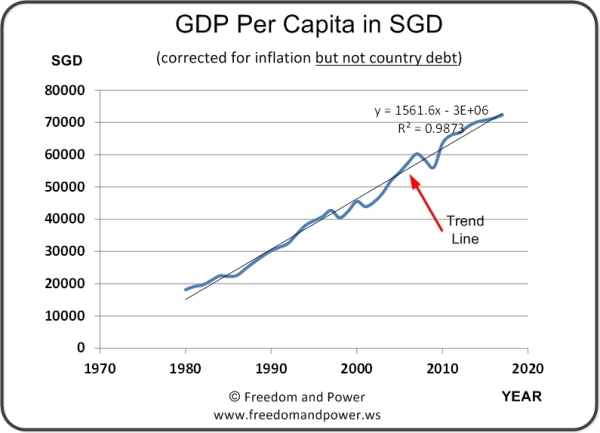

Sure. And that's what matters, right? Not only the economy is OK but it remains stable and growing. We can see this in the following chart:

It is plainly obvious that the minimum interventionist policy of Singapore since 1980 has had a very positive effect on the economy.

What this chart indicates is that since 1980 Singaporeans have seen their standards of living going up and up and up more or less in a linear fashion (take a look at the trend line in black). In technical terms, what we have here is the GDP per person corrected for inflation but -critically- not for public debt (we explain this below). This is so because we are only interested in the net accumulated wealth.

Yes, we know, this is not the greatest and more accurate statistic we can come up with (we could discount the money printed by the Singapore Central Bank, taxes and add many other corrections as we know that the GDP Keynessians Vodoo Economics, but let's not push it). For any intent and purpose this chart is eye popping.

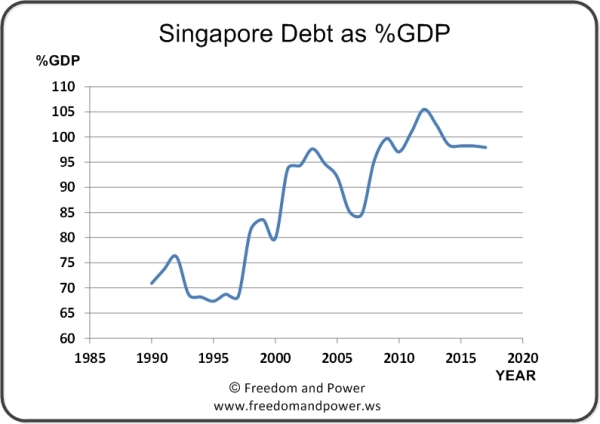

Also look at this one:

This is telling us that the Singapore debt (as a percentage of the GDP) has been increasing madly since roughly 1990, where it was already astronomical!!!

Is this proof that Keynesianism works, that debt is good to "stimulate" the markets? Is the Singaporean government borrowing and spending to prop-up their own markets? Is the Singaporean government doing what we have been explaining about time and time again; that anything is sustainable for as long as there is money to burn?

Are we soooooo hypocritical?

Well…no.

As we mentioned above, Singapore truly is an exception within "developed" economies. It so happens that Singapore not only has budget surpluses but they don't use borrowed money to prop-up their markets or for "social" needs. They use this money purely as investments which are fully backed by assets. Think of it this way, would you say that you are in debt if you have a debt of 10.000.000 EUR but you own property for 10 million EUR? Of course not. Your net debt would be 0.0 EUR. It is for this reason that we did not deduct government debt from the GDP per capita in our calculation above, simply because there is no debt; it's already paid for.

Now, having said that, do we believe that debt is good? Particularly government debt? Absolutely not and for a simple and very good reason. Government debt is entirely in the hands of politicians. There is no guarantee whatsoever that politicians won't be tempted to mis-use such a debt for "other" purposes (i.e. to "stimulate" the economy). So far Singaporeans have been lucky, but there are no guarantees. It is the old problem of Who Watches the Watchers. However, this article is not about government debt but about a country which can be approximated to free markets (again, more-or-less, within certain limits).

Think of it in this fashion. Singapore is using debt -to a large degree- to develop a Singaporean bond market. They do so because they want more investment money to pour into Singapore and as such they want the money to stay in Singapore. However, from a free market perspective this is highly inefficient. If you are an entrepreneur who is attempting to open an enterprise in Singapore, why would you borrow from a Singaporean market which is small and with higher interest rates if you could borrow from a much larger market with lower interest rates such as London or New York? Because the Singapore government -in a way- is forcing you to do so. See what we mean? What the Singapore government is doing only makes sense in an isolated environment with arbitrary rules which force you to accept less-than-optimum borrowing conditions.

Note: please see the Glossary if you are unfamiliar with certain words.